Sorry for the crappy quality of the photos above – the lighting in my apartment is not great.

A huge focus of mine over the past year or so has been reducing those blasted balances of mine. You saw in my last post on debt what those balances are. However, I have a question I’ve been trying to mull over.

My liquid savings right now is only about $2200. That includes my emergency fund. It’s just about one month’s expenses including loan payments (and that’s two loan payments of only interest accruing. Only one student loan payment bites into the principal, right now.) I don’t count anything I have saved for retirement as being liquid.

I think that part of my frustration right now is the feeling of being stuck. Of knowing you have a goal but also knowing its a little ways down the line, if you are realistic about things. I’ve already decided I will likely be making my move one before all the student loans are paid off. But I want to have a comfortable savings set aside too.

So, with the government being so messed up, and the interest rates remaining low, a part of me has mulled over the idea of saving like a banshee once the personal loan is paid off. Still making triple payments on the loan payment that is biting into principal, but taking the money I now attribute to my personal loan payments monthly ($354), and instead allocating it to my emergency fund and my tiny house/land account. (To make triple payments on that private loan means paying about $540 on it each month.) That way, I can feel less stuck, and encouraged at seeing something actually grow in a positive manner. And a balance going upward–imagine that!

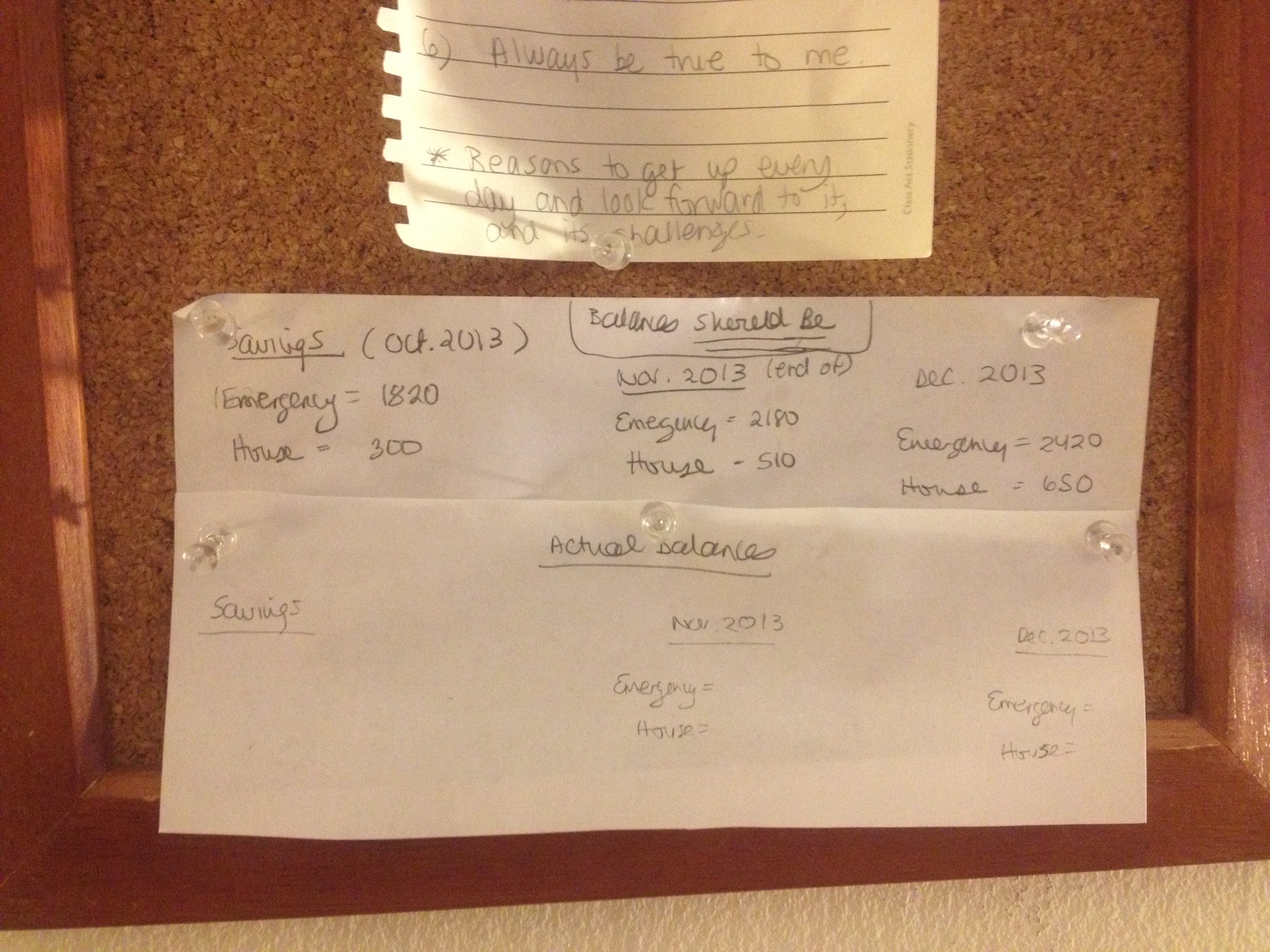

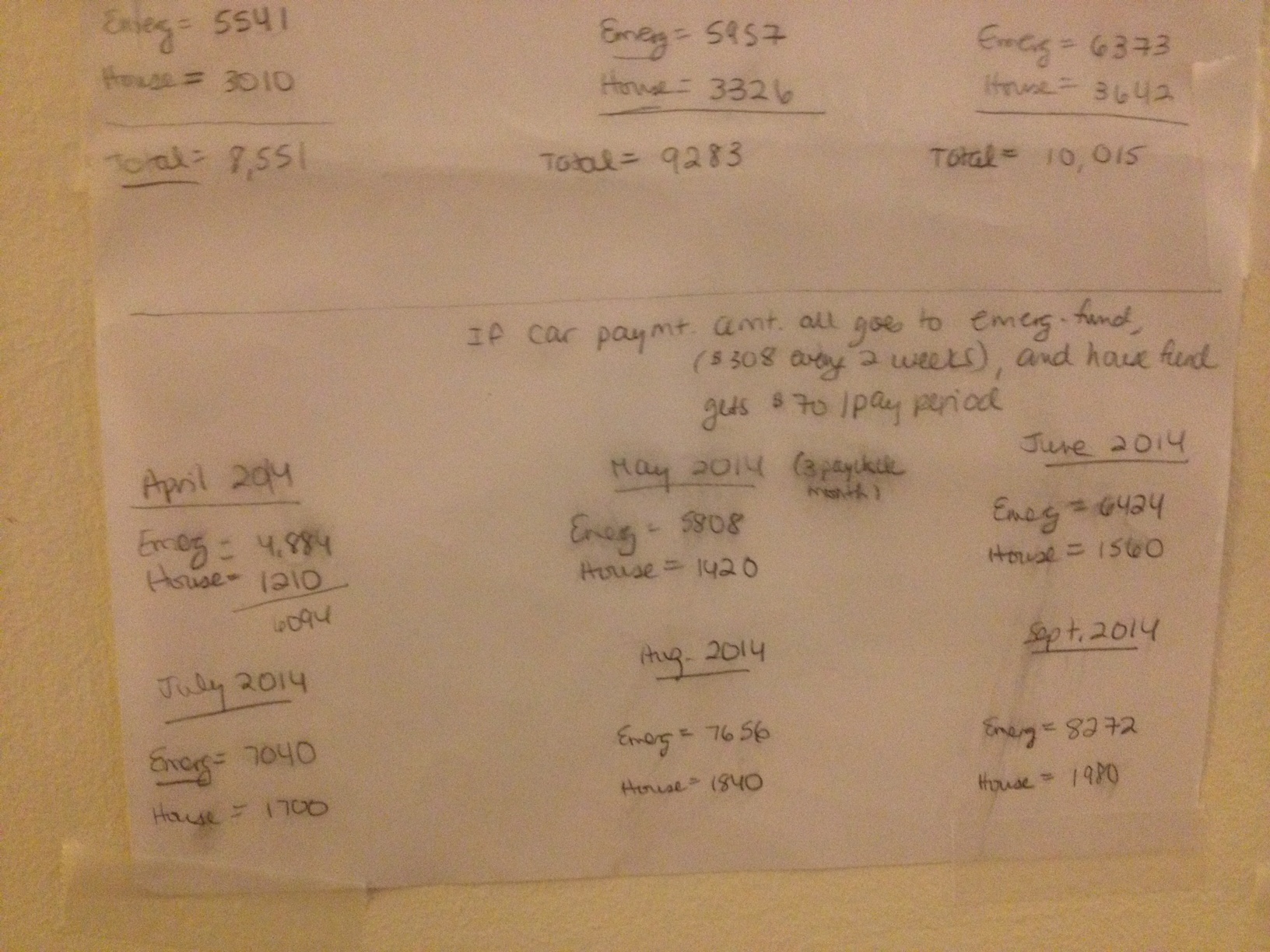

I have been listening to a lot of YouTube videos and understanding more of our Fed’s creation of cash currency as a Ponzi scheme of sorts, and it worries me to not have more set aside that I can readily get to. To that end, the other day I literally sat and wrote out two alternate scenarios for the upcoming year, with different allocations to each fund, to see how the balances could (and should) develop over time. Seeing the numbers in front of me made me feel better. A wee bit empowered, even. Again, imagine!

I put them all on my wall and I already feel like I’m making progress. I plan to take note (with various colored pens), as to whether each goal is met on a monthly basis. I am hoping to create a line graph showing my progress, showing the actual balances as compared to the “should be” balances. With any luck, those lines will literally be on top of each other. I’m definitely a visual person, and they always say writing things down helps. It totally does. I also started putting together a graph for the next three years, as I think that is now my goal time period in which to make a move. I want to set either monthly or quarterly goals, so I will feel like I’m continuing on my way, and can see measurable changes over time.

I’ve also started journaling on a more regular basis. Getting up earlier and writing in my journal really helps focus me. Also getting up early to get these posts done. To me, it is time well spent. I hope you agree.

What do you think about my plan to start saving like a banshee in January? Please leave a comment below on that or any other thoughts you might have! Thank you!

I love the visual graph! I use spreadsheets and have even done pie charts but the graph is epic! Your goals are lofty but totally doable as you’ve proven so far. Your honesty and openness are inspiring me to move ahead. Great job!

Why, thank you! And yes, I am a totally visual person, and not so good with excel, ergo, the pen and paper drawn chart! And I’m glad to inspire you – ditto right back at you!