I’ve noticed that people tend to really like these posts on my blog, and I hope it’s because my progress inspires people. This has been a really tough winter in the northeast – ridiculously “butt cold” temperatures and when it does warm up, it’s just to snow. (See my evidence in the pictures above.) So, I needed a pick-me-up to make me feel good. I have been meaning to chart my progress on my wall, so I gathered up the numbers.

Here’s how they look since I started really keeping track:

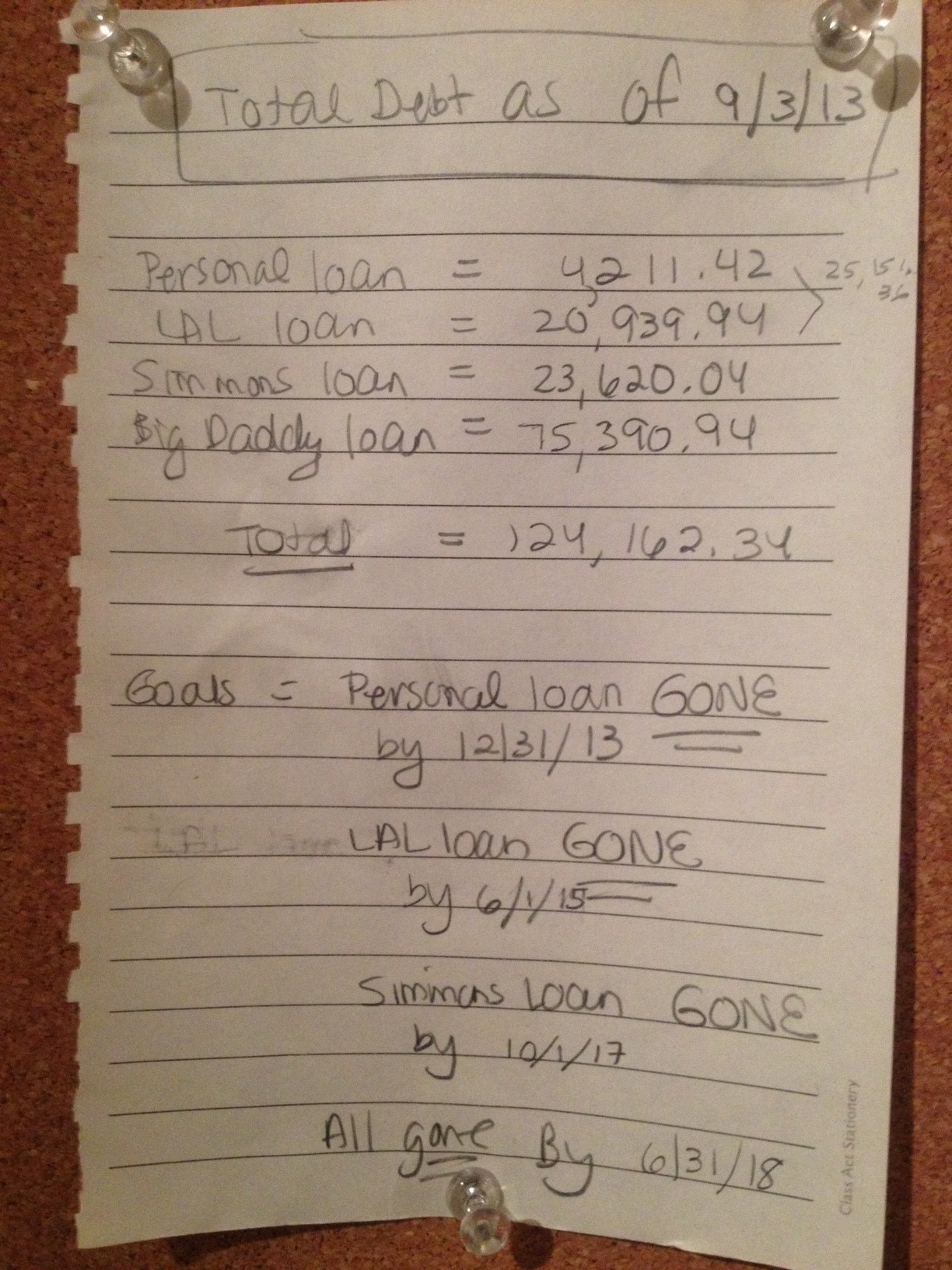

Sept. 2013:

Personal loan: $4,211.42

LAL loan: $20,939.94

Simmons Loan: $23,620.04

Big Daddy (federal) loan: $75,390.94

TOTAL BALANCE: $124,162.34

Today:

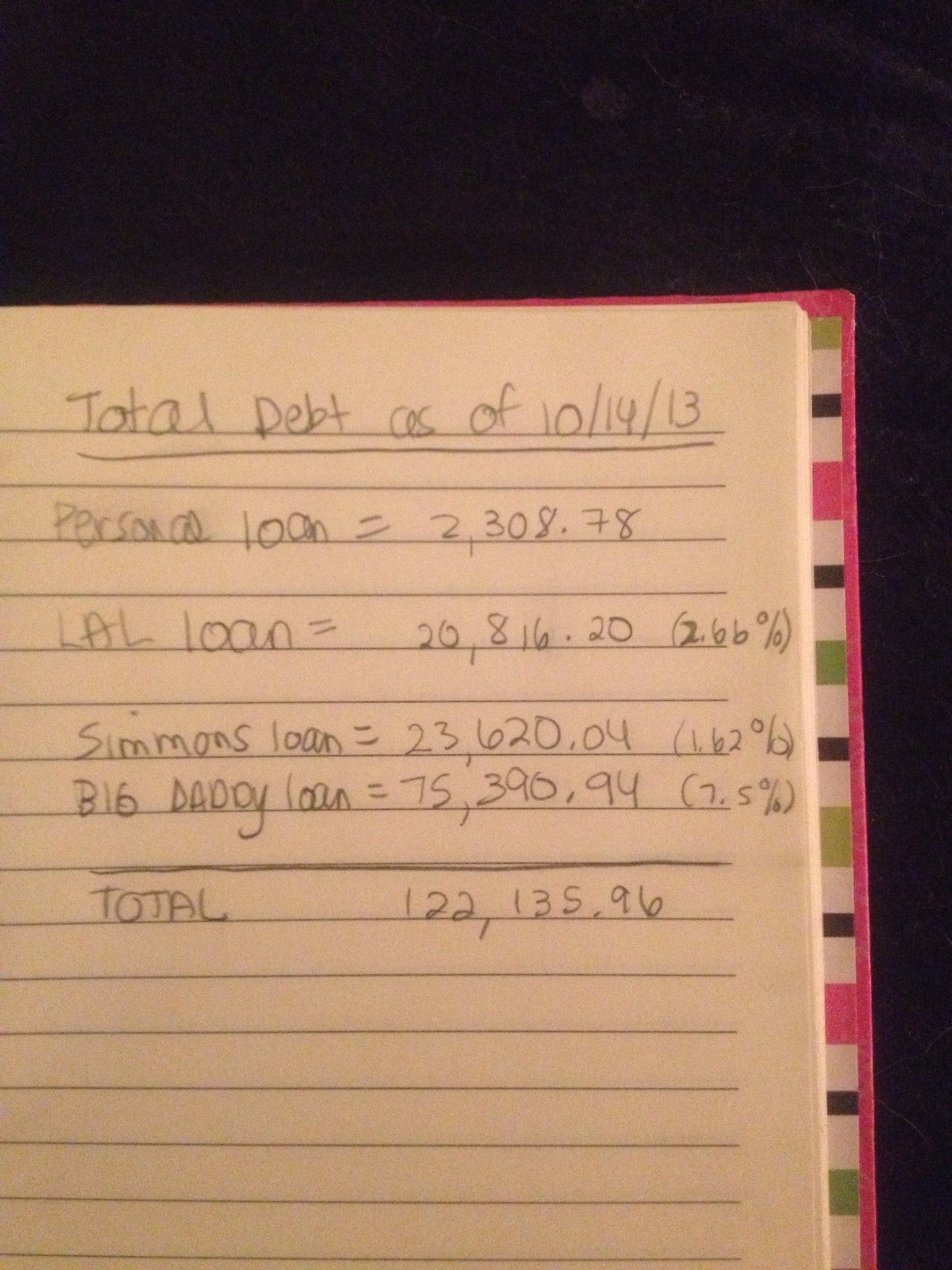

Personal loan: $000000000 (gone, gone, gone!!!!)

LAL Loan: $18,871.05

Simmons Loan: $23,620.04

Big Daddy (federal) loan: $75,390.94

TOTAL BALANCE: $117,882.03

DIFFERENCE (DECREASE in DEBT): $6,280.31 🙂 🙂 🙂

Of my last two payments on my LAL Loan ($455 and $171.95, respectively), here’s how much went to principal and how much went to interest:

$455 total payment = $397.46 to principal and $32.54 to interest

$171.95 total payment = $169.12 to principal and $2.83 to interest

I cannot tell you how happy this makes me!!

It’s been 5.5 months and I’ve gotten rid of more than $6K in debt, AND have increased my savings accounts to more than what they have ever been before since I’m on my own. I’ve gotten rid of enough shit in my apartment that I can now keep all of my christmas decorations here instead of taking up space in my brother’s attic. I’ve gotten a job at the gym which has been a goal of mine, and I start this Thursday evening. I’ve taken an additional test with NASM and passed, and am working on test #3 and certification #2. Out of nowhere, “my” author has asked for my help again on her book, and she really respects my work (and sense of humor) and pays me well for my time. I have a positive net worth due to my retirements savings and am continuing to put in more than 6% of my salary into my 403(b) account on top of the 10% that my employer puts in a pension (yes, really, I have one) plan, in which I am fully vested. Things are coming together!!

(To my friends out there reading this, if I ever get down on myself, could you remind me to read this post? Thanks.) As my brother said to me on facebook the other day “Sis, you’re doing it!”

You may have noticed that two of those loans don’t appear to have changed, balance-wise, since I embarked on this course. Today, that changes. You see, when I had more debt, I asked my lenders to allow me to just pay the interest that kept accruing on my loans per month. That equals $558/month. Yes, it’s depressing as hell to think about paying over $6,000/year just to keep a loan from growing. I’m calling my lender today and will be asking them to put me back on the standard repayment plan, so at least some of my payment goes toward cutting down the balance. It may not be much, but as I have learned, every little bit helps.

Good things are happening. I don’t know how or why but as I say to some of my friends when they question why things start going their way, “do not question the wisdom of the gods, just go with it.”

And now, for those of you who love the snow, I leave you with one more image. If I had been standing next to this snowpile (which wasn’t created by plows, etc., it was just there, it would have at least been up to my waist.)

If you liked this post, please like or subscribe!