I started writing this post about a month or so ago. It’s funny how some blog posts seem to pour right out of me like a thunderstorm, and others are like so many of the storm clouds I see around where I’m living right now. They hang around and you think something’s going to happen, and you get excited thinking about it all day long (that is, if you like storms like I do), and then at the end of the day, nothing, nada, zip. Just a bunch of dark clouds.

So… I’ve been doing a lot of thinking lately. About what I really value in life and what I think is wrong now and what can be fixed, etc. I think for a bit there, I was fighting a relapse into depression. I was avoiding going to see a doctor because I was worried the visit would cost me several hundred dollars since I have a $750 deductible with my insurance plan. I’d been rationing my prozac supply so it could last as long as possible. But the 20 mg is just not enough, I know that now. I was beginning to feel more like when I was first officially diagnosed, right after my husband and I split. It was not as severe, but it definitely didn’t feel right, or good. So I started taking 40 mg.

I also decided to go to a nurse practitioner, thinking the office visit would be less than seeing the doc in charge. I also asked for a new prescription for Wellbutrin. Using the two in combination worked for me in the past. I remembered how I used to feel confident about myself, and even happy. It’s been a few weeks now since I’ve been on the 40 mg and the wellbutrin, and the combo seems to be working well. A few days ago, on a drive home from Flagstaff with a friend, I looked out the window at the nighttime landscape and remembered, “this is what it used to feel like. When I was confident and felt at peace about stuff.” It’s just that it’s different now. Now I’m living that part of my life I was only thinking about doing, then.

If you’ve never experienced clinical depression, you might wonder how I knew. What were the warning signs? Well, I knew I was relapsing because I’d been starting to feel stressed about one item, and then my mind would let loose and start stressing about other things. It would start what I can only describe as a spiraling effect. Anti-depressants like Prozac help in that they help your mind to take a moment to say “wait, stop, think about what is really going here…think logically, not emotionally.” The Wellbutrin works with another part of your brain, because sometimes Prozac, in helping you to calm down and think, can also make you feel kind of blah. (At least for some people.) So Wellbutrin helps to counteract that. You can feel more pleasure in your life. It’s not a happy pill, though. You still have to do the work on yourself. I was also finding that I wanted to just go to sleep at night, or I was having problems getting up in the morning. The idea of working out in the am just sounded exhausting. I didn’t see any point in doing anything.

So that is one decision I made. I acknowledged what was going on with me, inside, and decided to do something about it.

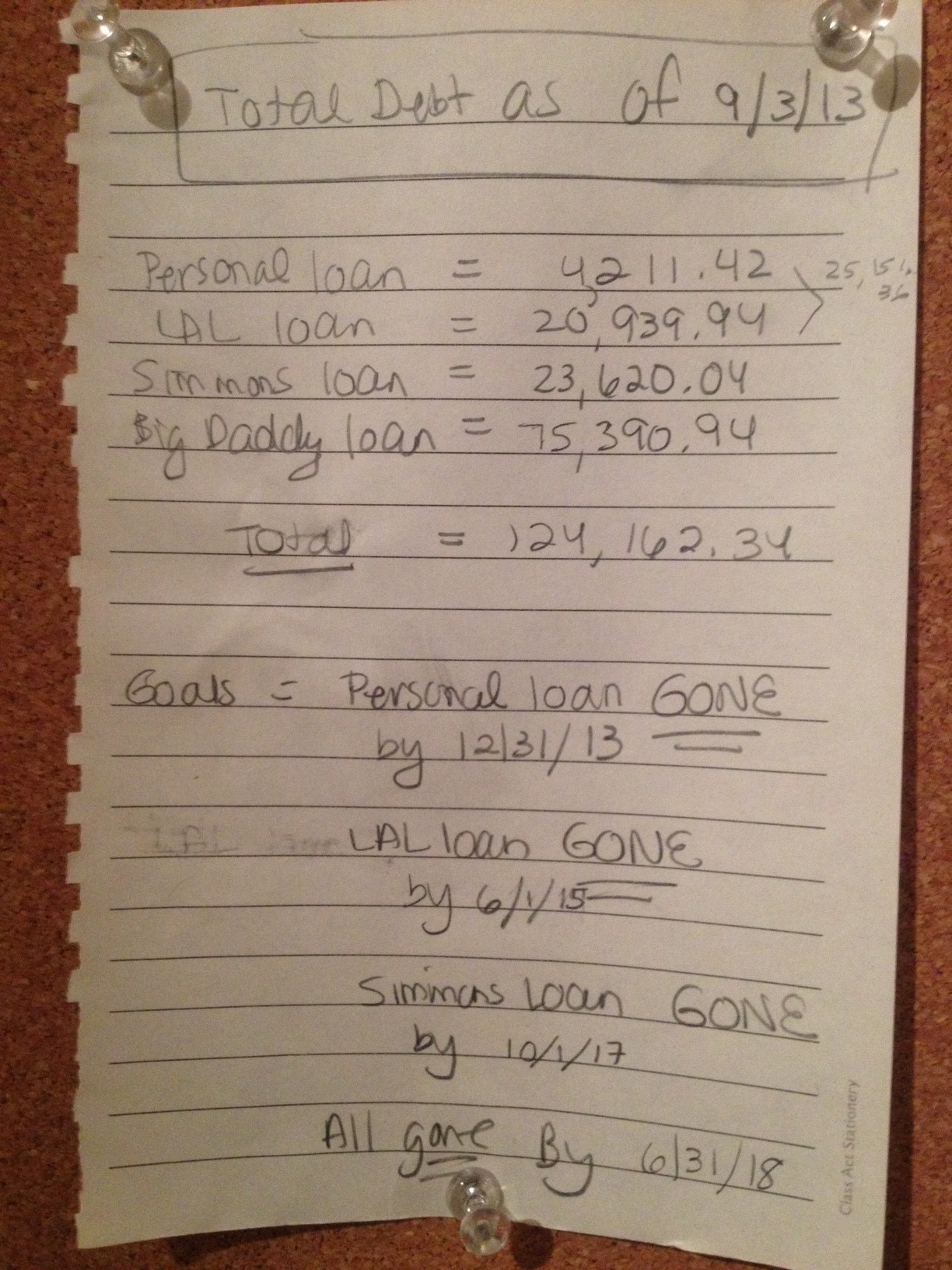

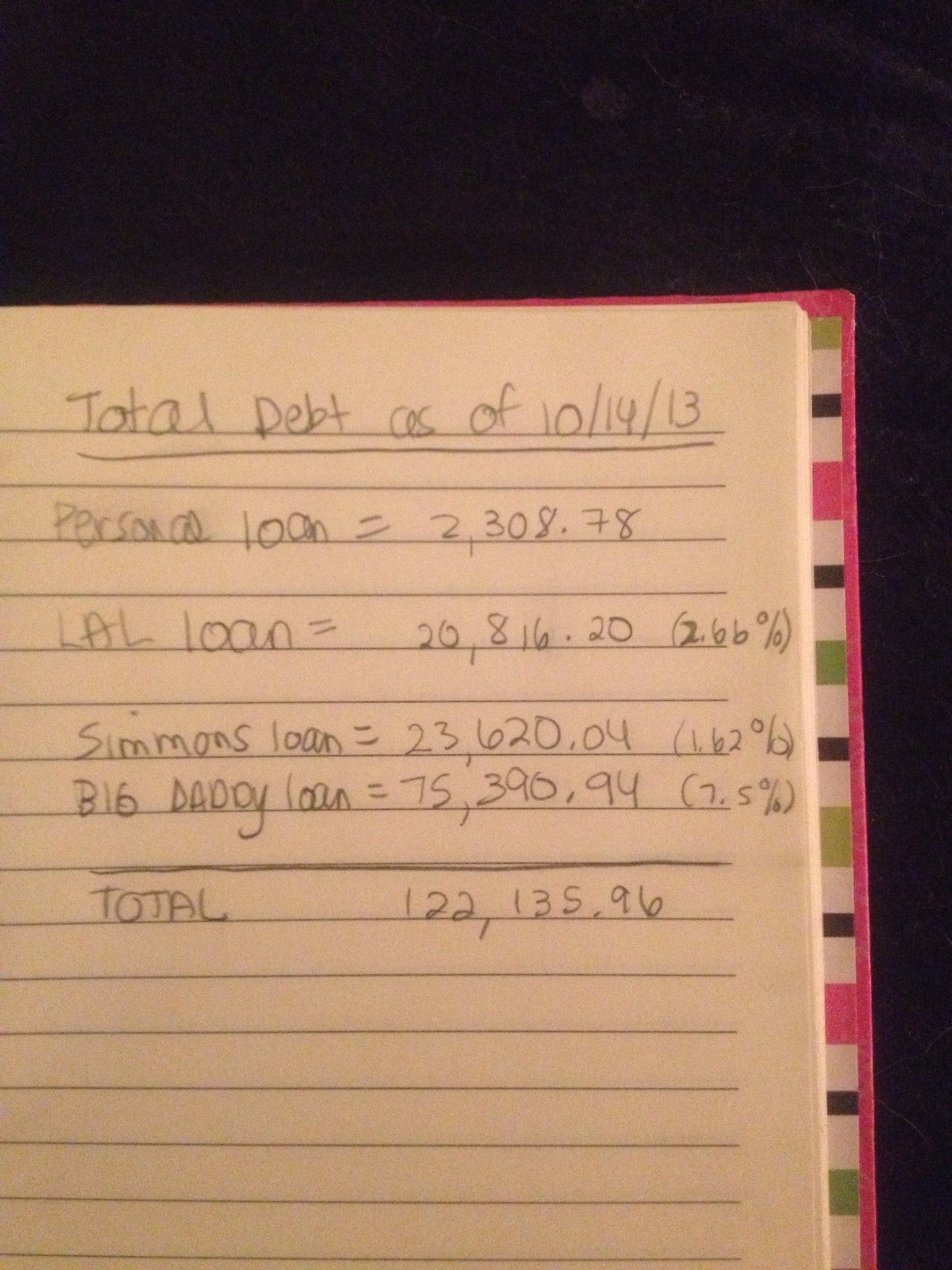

Debt. Well, yes, I have it again. A credit card balance. I did have two – I decided to take some money out of savings and pay off one of them – the one that was accruing interest. And that credit card has gone into the freezer. It is encased in a HUGE block of ice in a mason jar. The other card has a zero percent interest rate for 21 months, so now it’s time to chip away at it. I’ve also put a savings thermometer on my wall so I can track my progress. It’s posted right near the door so I see it everytime I leave for work.

Other decisions have not been so cut and dry and not so much set in stone. Yes, I know I want to leave this area by the time my lease is up, if not before. But as to where I’m going, thas been in flux. When I first started writing this post, I had decided, “that’s it, I’m moving back east.” I was so decided that I even posted about it on facebook. Because, you see, that’s how I hold myself accountable (usually.) I put it out there and then feel like I have to follow through with it. But here’s the thing. That’s the kind of thinking that got me into a lot of trouble with certain decisions in my life. The idea that because I had started law school, I had to finish it, no matter how miserable it made me. The idea that I needed to stick it out in my marriage when I was so unhappy, because that’s what was expected of me, and what I expected of myself, because that’s what you do. You stick things out and make them work.

I’m realizing now in life, though, that things don’t have to be set in stone. Decisions can be made and decisions can be changed. I don’t have to have everything always figured out and planned ahead of time. And just because I decide to change up on things doesn’t mean I am a quitter or a failure. I don’t know why I have always been so hard on myself. I just have.

I’m realizing maybe the southwest isn’t so bad after all – maybe it’s just the location where I am now, or the fact that it’s such a small town and such an extremely different from where I spent so much of my life, that has made me feel like a fish out of water. I said to a friend recently, I feel like in this town, I’m just a visitor. I don’t feel like I really, and truly, belong here. So I’m going to try out other places in the southwest, even if it’s just with a few trips. I’m going to road trip to Albuquerque when the season is over (at least that’s the current plan) to check it out. It looks like a city where the cost of living is a lot less expensive, the food is amazing, the winters are a lot milder than back east, the city is surrounded by beautiful mountains, lots of running and hiking trails, there are universities and colleges (and therefore, more options for jobs should I go that route) and a lot of diversity. I know not everyone likes it there (Jen, are you reading this?!) but that doesn’t mean that I won’t.

I’ll be honest, folks. I am SICK and TIRED of living in expensive places where I spend so much time worrying and working to pay rent. Yes, I know there will be shitty areas of town wherever I look, as there are shitty areas of town in any city in this country. As long as I can afford to not live in a horrible section, and feel safe when I sleep at night, I consider that a positive. In fact, I will look for the smallest place possible, because as you know, I don’t like a bunch of extra crap in my life. If I question getting something, I just ask myself, “Do I want to move this in the future?” That kind of question really helps you to prioritize possessions.

I’ve decided to get back into working out regularly. A friend and I individually used to work out 5-6 days per week, and neither one of us can stand how we feel. I’ve begun running again, and just the other day, bought myself some new Hoka One One Running Shoes (the Clayton model, to be exact.) And I made sure I could afford them since I’ve worked so much overtime lately. I’m headed to the gym this morning to run on the treadmill a bit, and then do some weights. Tomorrow, I’ve been invited to go canyoneering which is exciting and terrifying at the same time since it involves rappeling and I do have a fear of heights. But I’ve pushed through that kind of fear before when I learned how to do top roping, and I remember the feeling of confidence it gave me afterward. I need to continue pushing myself out of my comfort zone. And I really do want to see other parts of this area where I live. It’s not safe to go hiking by yourself in the desert, which is why I’ve felt constrained and unhappy, not being able to do it before now. So, I’m glad to have the opportunity to do it tomorrow. If you see another blog post from me, you’ll know I’ve survived. 🙂

Anyway, again, sorry for the long delay in posts. I hope I haven’t worried some of you with my silence.