Working on saving these so I can owe less of these…

Two Christmases ago, I remember thinking to myself, “this sucks. I have less than $500 in savings, over $7000 in credit card debt and can’t even charge anything even if I want to because it will put me over the limit, and I have less than $30 in my checking account. HOW did I get here? I’m 39!”

Yes, I look at this moment as my financial rock bottom.

Today, my savings account is much healthier, and I can afford to rent a car this week to go home for Thanksgiving. (I found out Budgetwill let you rent without a credit card if you fit certain qualifications.) I have zero credit card debt (and zero personal cards–the only credit card I have is a corporate one.) I have $1169 due on a personal loan and I will have that paid off by Dec. 31st, “come hell or high water” as my mom used to say. The only debt remaining will be my student loans. Read more →

Click on the image to enlarge – this is the beginning of my line graph!

Click on the image to enlarge – this is the second part of my line graph!

Sorry for the crappy quality of the photos above – the lighting in my apartment is not great.

A huge focus of mine over the past year or so has been reducing those blasted balances of mine. You saw in my last post on debt what those balances are. However, I have a question I’ve been trying to mull over.

When I wrote my earlier post about fear, my friend Kate said maybe I should turn my fears on the side and take a look at how far I’ve come. I definitely want to do that. But for tonight, I’m going too take a look at how far I’ve come in getting rid of my debt in about 6 weeks. It helps me to see it in perspective like this. It is working. Just not as fast as I might like it to move.

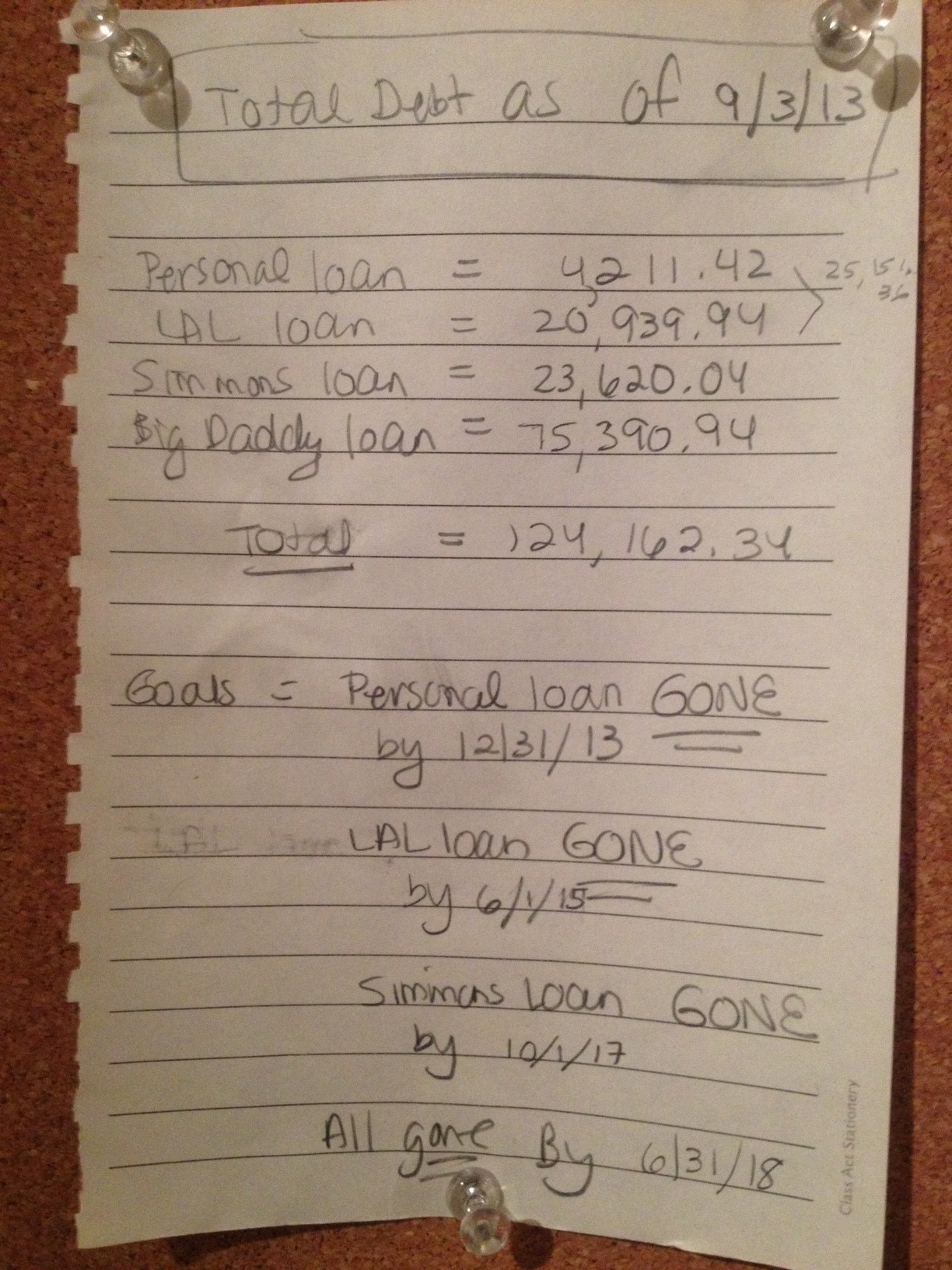

Here is a picture of my overall debt as of Sept. 3rd of this year (just click on the photo to enlarge):

Total Debt as of Sept. 3rd

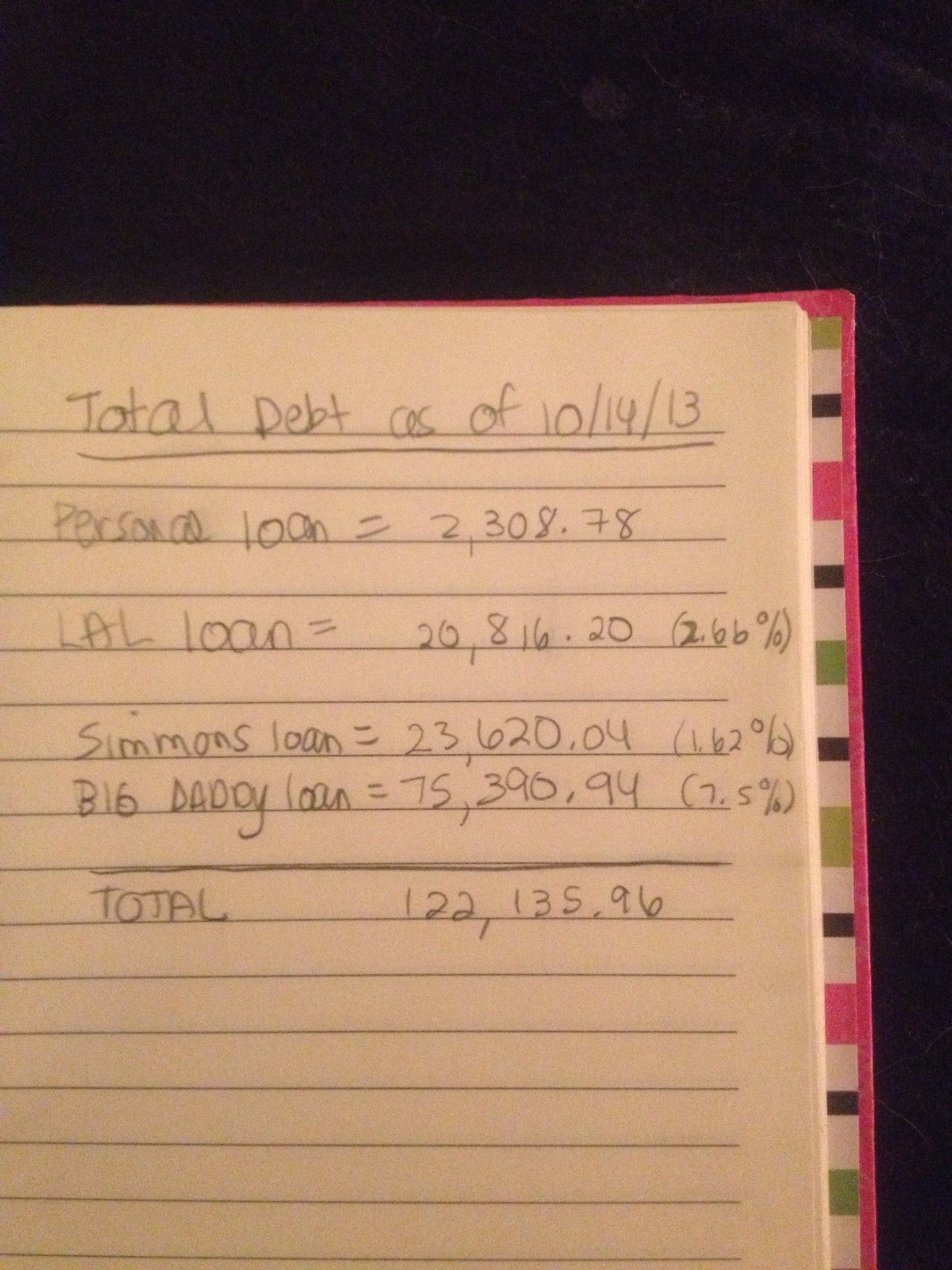

And here is a picture of my debt as of October 14th ((just click on the photo to enlarge):

Total Debt as of October 14th

I think this is good considering it’s only been about 6 weeks. The difference amounts to $2,026.38!! And yes, I really have nicknamed one of my loans, Big Daddy. And yes, that’s a fixed interest rate of 7.5%. I know….sigh….

You might wonder how I don’t paralyze myself by looking at these numbers. Well, I try to not look at them as a whole. I try to focus on the little gains I am making in them month to month. My LAL loan has a variable interest rate that can go as high as 9%, so it’s my next area of focus after my personal loan is gone. That and establishing more of an emergency fund than what I currently have. Then, Big Daddy and then finally the Simmons loan. (My financial advisor suggested this order.)

There is a line in one of my favorite YouTube videos where Logan Smith makes the point that people always think that they need to earn more money, but they forget that “they can always spend less.” He emphasizes the word “less.” That made a big impact on me. It’s part of why I sold my car. It’s why I don’t eat out much, especially for lunch at work like many of my colleagues. I can eat healthier if I bring my own from home. The few times that I have bought lunch at work is when someone is quitting and it’s a good-bye lunch. And dinners, I usually eat at home also. And all those books that discuss the “latte factor?” Yeah. Those don’t apply to me either.

While i have taken Logan’s words to heart, I am also looking for ways to increase my income. A friend of mine, whose husband is out of work, told me about mystery shopping. I just signed up with a few companies over the weekend and have already received some emails about “shops” in my area. I’m excited to try it out, and hope that there are opportunities to do more than pose as a buyer at a car dealership (what i have already seen posted.)

One thing I like about the concept of mystery shopping is the freedom you have in scheduling your shop. You get a date range during which the shop should be done but the actual scheduling ultimately works on your own schedule. I’m hoping I can make a little bit of extra money to out aside for my tiny house (or just pay off debt faster), but I need to make sure I still have time for studying and writing, as well as my furballs. I don’t want to lose sight of my priorities in addition to getting rid of my debt.

This doesn’t take into account any money I am trying to save. It’s hard to do both – save and drastically pay down debt simultaneously. But I’m trying! (That’s for another post — I’ll keep this one short.)

Stay tuned, I will let you know how it goes, on both the debt reducing and the mystery shopping fronts!

Photo courtesy of MyBike.com, from whom I will be ordering it

Well, I finally made it through my decision impairment and have made a choice. (Whenever there is a large amount of money involved, it can take me a long time to decide things.) After a LOT of research, I have decided to buy an electric bike, and I will be ordering it on Friday as soon as I get paid. Read more →

Cape Kiawanda, part of Three Capes region on Oregon Coast

Through my Everyday Magic online photography course, I’ve seen some absolutely beautiful, breathtaking images. I notice that my favorites tend to be of the west coast. The above photo I took a few years back when I was on the Oregon Coast, driving southward from the Cannon Beach area. I haven’t touched up the image, but can’t wait to play with it with some of my camera apps!

Have you ever felt this pull to be somewhere else? And felt it your entire life? As many years back as I can remember, I have wanted to be there. I remember both of my trips down the Oregon Coast like they were yesterday even though one took place almost 20 years ago. I took the first with an old friend, and the second one all on my own. Both have seared images into my brain. I rememeber how my friend and I felt that first time we hit the Pacific Ocean, with all of the sea stacks jutting out from the water. On the the second trip, I remember sitting near Cape Perpetua for several hours, just watching the waves crash onto the shore. Read more →

Last week, I wrote that I started to cut away at my debt by ceasing to buy crap I didn’t need. That’s only part of the equation. I have also gotten rid of a lot of stuff that I found I didn’t use. Some of it, I gave away via freecycle.org. Other things, I sold on Craigslist. Things I sold:

I think that most people know and understand that it is much easier to pay off debt if you are married or in a relationship than when you are single. When you are married, you have that second income to fall back on. At least, that’s the way it was for me until about three years ago. Read more →

In fact, one of them could be getting ready to go off to college. The youngest could be shopping for back to school clothes for fifth grade and the middle “kids” would have just gone to their first prom a few months ago. No, really. I have to say, I am ready to have “empty nest syndrome” where my student loans are concerned. Read more →